At present, the macroeconomic situation is stable and the output of steel mills has rebounded. According to the statistics of the China Iron and Steel Association, the daily output of crude steel of key enterprises in the first half of November was 1.763 million tons, which was a month-on-month increase of 3.5%, and the national estimate was 2.144 million tons. This was a 2.2% increase from the previous month, while the steel market has entered the off-season and the market demand has been gradually reduced. It is expected that the domestic steel market will continue to fluctuate this week (2013.11.25-11.29).

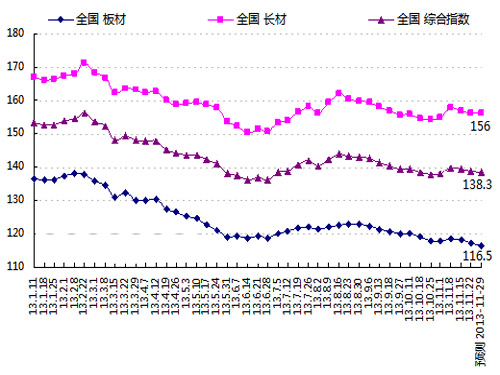

At present, the macroeconomic situation is stable and the output of steel mills has rebounded. According to the statistics of the China Iron and Steel Association, the daily output of crude steel of key enterprises in the first half of November was 1.763 million tons, which was a month-on-month increase of 3.5%, and the national estimate was 2.144 million tons. This was a 2.2% increase from the previous month, while the steel market has entered the off-season and the market demand has been gradually reduced. It is expected that the domestic steel market will continue to fluctuate this week (2013.11.25-11.29). According to the Lange Steel Information Research Center weekly price forecasting model data, this week (2013.11.25-11.29) domestic steel market prices will continue to fluctuate and decline, long product market prices will fluctuate slightly, and the plate market price will decline steadily or slightly. Lange Steel's national comprehensive steel price index is expected to fluctuate around 138.3 points. The average price of steel is around 3,600 yuan, with an average fluctuation of around 20 yuan. Among them, the long product price index is expected to fluctuate around 156 points, with slight fluctuations of about 0.2 points. The price index is expected to fluctuate around 116.5 points, with slight fluctuations of around 0.7 points.

Lange Steel Information Research Center market survey data show that this week (2013.11.25-11.29) domestic long products market prices will fluctuate slightly, the market price of sheet metal will steadily decline 3; raw material market prices will fluctuate slightly, iron ore market prices With small fluctuations, the coke market price will stabilize steadily, the scrap market price will drop slightly, and the billet market price will remain stable.

1. Domestic steel market continued to decline this week. Week 47 of 2013 (2013.11.18-11.22) Lange Steel's national comprehensive steel price index reached 138.7 points, down 0.43% from the previous week and 6.71% from the same period of last year. Among them, the LGMI long products price index was 156.2 points, down 0.45% from the previous week and 4.62% from the same period of last year. The LGMI sheet price index was 117.6 points, down 0.38% from the previous week and 9.87% from the same period of last year. 1).

According to the market monitoring of Lange Steel Information Research Center, in the 47th week of 2013, the prices of iron and steel raw fuel and steel products in 17 categories and 44 specifications (varieties) in some parts of the country were changed as follows: Market prices of major steel products continued to decline slightly. Compared with the week, the rising varieties increased significantly, the flat varieties decreased, and the falling varieties decreased slightly. Of these, 9 varieties rose, compared with the previous week, an increase of 7 species; 19 species were flat and 4 species decreased compared with last week; 16 species fell, 3 species decreased compared with last week. The prices of domestic steel raw materials market were mixed, iron ore market prices fluctuate slightly, coke market prices remained stable, scrap market prices fell by 20-30 yuan, and billet market prices increased by 10-20 yuan.

2. This week, the steel market oscillated and rebounded. In Week 47 of 2013 (2013.11.18-11.22), the main contract for the rebar ** market continued to show signs of sluggishness, with many intraday volatility patterns, although this week it rebounded. However, there has been no clear upward trend. This week's closing price has rebounded by 21 points from last week. Although the price has been reversed, the rebounding road is quite tortuous, causing people to worry about the room for rebound. This week, the main 1405 positions held 1.624 million contracts, an increase of 22,358 lots, and the positions did not change much. Funds were conservative about the current situation. Repeated dishwashing of intraday prices also increased the difficulty of operation.

3. This week, the nation's steel stocks have been continuously declining. At present, the nation's steel stocks have declined for 6 consecutive weeks, and the decline rate of building materials and sheet stocks have all slowed slightly. According to market monitoring by Lange Steel Information Research Center, on November 22, steel society stocks in 29 key cities across the country were 12.5184 million tons, a decrease of 119,100 tons or 0.94% from the previous week, slightly lower than last week's rate of decline. A slowdown of 0.52 percentage points. From the perspective of sub-categories, the country’s wire rod social inventory is 1,060,500 tons, down 2.31% from the previous week, a slight slowdown of 0.70 percentage points from the previous week's decline, a decrease of 14.52% from the previous month and an increase of 6.59% from the same period of last year. Rebar social inventory was 4.5454 million tons, down 1.09% from last week, a slight slowdown of 0.85 percentage points from the previous week's decline rate, a decrease of 9.00% from the previous month and an increase of 2.57% from the same period last year; The amount was 331,800 tons, which was 1.97% higher than last week. It changed from last week's decline to increase, 6.46% from the previous month and 32.24% from the same period of last year; the social volume of hot-rolled coils was 3,626,100 tons. Weekly decrease of 0.90%, a slight increase of 0.43 percentage points from the previous week's decline, a decrease of 4.11% from the previous month and an increase of 12.02% from the same period of last year; the volume of CRC's social inventory was 1.5608 million tons, up 0.01% from last week. From last week’s decline to increase, it was down by 1.25% from last month and 0.62% from the same period of last year. The plate’s social inventory was 1,393,800 tons, which was 1.23% lower than last week, slightly lower than last week’s decline rate. 0.75 percentage point slower than the previous month, 6.25% lower than last year The period increased by 3.36%.

4. Focus on market factors this week Macroeconomics:

[Industrial Electricity] National industrial electricity consumption by 322.1 billion kwh in October increased by 8.5% year-on-year

According to CEC statistics, in October, the national industrial electricity consumption was 322.1 billion kWh, an increase of 8.5% over the same period of last year, and the contribution rate to the growth of electricity consumption of the entire society was 65.9%. Among them, light industrial electricity consumption was 52.3 billion kWh, an increase of 6.7% year-on-year, an increase of 0.4 percentage points over the same period of the previous year; heavy industry electricity consumption was 269.8 billion kWh, an increase of 8.8% year-on-year, and the growth rate was higher than the same period of last year. 3.0 percentage points.

From January to October, the national industrial electricity consumption was 3110.2 billion kWh, an increase of 6.6% year-on-year, and the growth rate was 3.5% higher than the same period of last year; the proportion of electricity consumption in the entire society was 71.7%, and the electricity consumption of the entire society increased. The contribution rate is 64.7%. Among them, light industrial electricity consumption was 526 billion kWh, an increase of 6.0% year-on-year, and the growth rate was 1.6 percentage points higher than the same period of the previous year; heavy industry electricity consumption was 2614.2 billion kWh, an increase of 6.8% year-on-year, and the growth rate was higher than the same period of last year. 3.8 percentage points.

[Industrial Electricity] In October, the electricity consumption of the four major high-energy-consumption industries increased by 8.6% year-on-year to 14.31 billion kWh.

According to CEC statistics, in October, the four high-energy-consumption industries used a total of 143.1 billion kWh, an increase of 8.6% year-on-year, an increase of 0.5 percentage points from September and an increase of 2.3% from the previous month; total electricity consumption The proportion of electricity consumption in the entire society is 32.7%. Among them, the electricity consumption of the chemical industry was 34.7 billion kWh, an increase of 5.8% year-on-year, and an increase of 2.0% from the previous period; the electricity consumption of the building materials industry was 28.3 billion kWh, an increase of 10.3% year-on-year, an increase of 1.9%; the electricity consumption of the ferrous metal smelting industry was 471 Billion kWh, an increase of 15.7% year-on-year, an increase of 3.3% from the previous period; non-ferrous metals smelting industry was 33.1 billion kWh, an increase of 1.1% year-on-year and an increase of 1.5% month-on-month. From January to October, the total electricity consumption of the four high-energy-consumption industries including chemical raw material products, non-metallic mineral products, ferrous metal smelting, and non-ferrous metal smelting totaled 136.3 billion kWh, a year-on-year increase of 5.6%; total electricity consumption occupies the entire society. The proportion of volume is 31.1%, and the contribution rate to the growth of electricity consumption of the whole society is 26.0%. Among them, the chemical industry used 328 billion kwh electricity, an increase of 5.0%; building materials industry electricity consumption 256.1 billion kwh, an increase of 5.9%; ferrous metal smelting industry electricity consumption 451.1 billion kwh, an increase of 6.7%; The metal smelting industry was 327.7 billion kwh, an increase of 4.6% year-on-year. The growth rate of electricity consumption in the building materials and steel industry was 5.9 and 12.3 percentage points higher than that of the same period of the previous year, and the growth rate of electricity use in the chemical and non-ferrous industry fell by 1.6 and 2.1 percentage points respectively.

[PMI] November HSBC China Manufacturing Purchasing Manager Index Preview Value 50.4

According to statistics of HSBC Holdings Limited, China's manufacturing purchasing managers' index (PMI) in November was 50.4, and the final value in September was 50.9. China's November HSBC Manufacturing PMI New Export Order Index was 49.4, a three-month low.

[State-Owned Profits] National SOE profits rose by 10.1% from January to October

According to statistics from the Ministry of Finance, from January to October, the main indicators of economic efficiency of state-owned and state-controlled enterprises across the country showed continuous growth, with a total realized profit of 1,970.78 billion yuan, a year-on-year increase of 10.1%. In the first 10 months, the central enterprises realized profits of 1,423.28 billion yuan, a year-on-year increase of 13.9%; and local state-owned enterprises reached 477.5 billion yuan, a year-on-year increase of 1.1%.

From January to October, the total operating income of state-owned enterprises totaled 3.7701 trillion yuan, an increase of 11% year-on-year. Among them, the central government had a total of 2,318.475 billion yuan, an increase of 9.8% year-on-year; local state-owned enterprises were 1451.6 billion yuan, a year-on-year increase of 13%. In the first 10 months, the total operating costs of state-owned enterprises totaled 36,279.03 billion yuan, an increase of 11.2% year-on-year, of which sales expenses, management expenses and financial expenses increased by 11.6%, 6.3% and 6.7% respectively. State-owned enterprises should pay taxes and taxes of 30029.5 billion yuan, an increase of 7.3% year-on-year.

From January to October, assets of state-owned enterprises totaled 8,947.09 billion yuan, a year-on-year increase of 13.4%; liabilities totaled 584,238.2 billion yuan, a year-on-year increase of 14%. The total equity of the owners was 309.927 billion yuan, a year-on-year increase of 12.2%. The Ministry of Finance stated that from January to October, the state-owned electronics, electricity, construction, real estate, transportation, and automotive industries achieved higher profit growth, and state-owned non-ferrous metals, chemicals, coal, machinery, and other industries realized large reductions in profits.

Industry News:

[Coal steel production for ten days] In the first half of November, the national crude steel output was 1.763 million tons, an increase of 2.2% from the previous month

According to statistics from the China Iron and Steel Association, in the first half of November, the daily output of crude steel of key enterprises was 1.763 million tons, up by 3.5% from the previous month, and the national estimate was 2.144 million tons, up by 2.2% from the previous month. At the end of the previous quarter, steel stocks stood at 12.926 million tons, up 0.39% from the end of the previous period and 23.5% from the beginning of the year.

Downstream demand:

[Manufacturing Electricity] National electricity consumption in manufacturing industry rose by 9.1% from 238.5 billion kWh in October

According to CEC statistics, the country’s electricity consumption in the manufacturing sector totaled 238.5 billion kilowatt hours in October, a year-on-year increase of 9.1%, an increase of 1.3 percentage points from the previous month; the national average daily electricity consumption of the manufacturing industry was 7.69 billion kwh/day. , a decrease of 340 million kWh/day from the previous month, the lowest month since April of this year. From January to October, the nation's electricity consumption for manufacturing was 2,239.3 billion kWh, an increase of 6.4% year-on-year, an increase of 4.1% over the same period of last year.

ZHITONG PIPE VALVE TECHNOLOGY CO.,LTD , https://www.ztpipevalve.com